Real World Examples

Contents

Real World Examples#

Utilities#

import sys

from pathlib import Path

parent_dir = str(Path().resolve().parent)

sys.path.append(parent_dir)

import random

import warnings

import matplotlib.pyplot as plt

import numpy as np

import scipy.stats as stats

warnings.filterwarnings("ignore", category=DeprecationWarning)

%matplotlib inline

from utils import seed_all, true_pmf, empirical_pmf

seed_all(42)

Using Seed Number 42

Call Center Simulation#

This example is taken from [Yiu, 2019], please take a look at this author’s articles, they are really good!

Imagine that we are data scientists tasked with improving the ROI (Return on Investment) of our company’s call center, where employees attempt to cold call potential customers and get them to purchase our product.

You look at some historical data and find the following:

The typical call center employee completes on average 50 calls per day.

The probability of a conversion (purchase) for each call is \(4\%\).

The average revenue to your company for each conversion is \(90\).

The call center you are analyzing has \(100\) employees.

Each employee is paid \(200\) per day of work.

Bernoulli Trials#

Let \(X\) be the success conversion call status of a call made by 1 single randomly chosen employee. In other words, let \(X\) be the outcome of a call made by 1 single randomly chosen employee where the outcome is either success or failure in conversion.

Then we can model the probability of success of a call made by a randomly chosen employee as a Bernoulli random variable \(X\) with parameter \(p\) where \(p\) is the probability of success of a call made by that randomly chosen employee.

We need to follow some assumptions in order to make \(X\) a Bernoulli Trial:

Each trial has two possible outcomes: 1 or 0 (success of failure);

This means any single employee can only make call that is successful or not.

The probability of success is constant for each trial, as mentioned, the probability of a conversion (purchase) for each call is \(p=0.04\). We treat is as constant.

This means everytime a call is made by a randomly chosen employee, the success rate is constant at \(p=0.04\).

Each trial is independent.

This means that each call made by the randomly chosen employee is independent of the previous calls made.

We define the sample space, event space and probability measure below:

The sample space \(\S = \{0,1\}\) where \(0\) represents failure and \(1\) represents success.

The event space \(\E = \{\emptyset, \{0\}, \{1\}, \{0,1\}\}\).

The probability measure \(\P\) is defined as follows:

\(\P(\emptyset) = 0\)

\(\P(\{0\}) = 1-p = 0.96\)

\(\P(\{1\}) = p = 0.04\)

\(\P(\{0,1\}) = 1\)

Our random variable \(X: \S \to \R\) can be defined as \(X(\{0\}) = 0\) and \(X(\{1\}) = 1\), or \(X(0) = 0\) and \(X(1) = 1\). The states of \(X\) are \(\lset 0, 1 \rset\).

Consequently, the PMF is fully determined by

\(X\) is a Bernoulli Trial because we can think of it as 1 single person tossing 1 coin, then the corresponding random variable \(X\) is the outcome of the coin toss made by 1 randomly chosen single person. Therefore, it can be made to fit as a Bernoulli Trial if we assume the assumptions as above.

Binomial Distribution#

Now the above details a single call made by a randomly chosen employee, which follows a Bernoulli distribution. You can associate this with a single coin toss made by a randomly chosen person, which also follows a Bernoulli distribution (i.e. \(X \sim \bern(0.04)\)).

Now, a single employee can make multiple calls. For example, in the example above, an employee can make 50 calls a day. We can define a sequence of calls \(X_1, X_2, \ldots, X_{50}\). One confusion that arise here is what each \(X_i\) mean. In this particular settings, it would be reasonable to assume that each \(X_i\) is a copy of \(X\) where \(X\) is the randomly chosen person. This means once \(X\) is determined (tagged to the person chosen, say person A), then \(X_1, X_2, \ldots, X_{50}\) all refer to this person A’s calls as it does not make sense that \(X_i\) correspond to different person. See here’s example on “Suppose that a student takes a multiple choice test” to see how they phrase it. I think I should rephrase the definition of my Bernoulli r.v. just now as the employee is not “random”?

Since each \(X_i\) is a Bernoulli trial, then \(n\) such calls are identically and independently distributed (i.i.d.), then we can define \(Y\) to be the number of successful conversion calls, which now follows a Binomial distribution because each call made by the employee is \(\iid\) and follows a Bernoulli distribution with constant parameter \(p\).

Since \(n=50\) and \(p=0.04\), we can define our \(Y\) as follows:

So \(Y = X_0 + X_1 + \ldots + X_{50}\) in this scenario, note \(Y\) is still made by 1 single employee. It is just the total number of successful conversion calls made by 1 single employee.

Each call by 1 single employee is \(\iid\), this means it is similar idea to 1 single person tossing 1 coin 50 times.

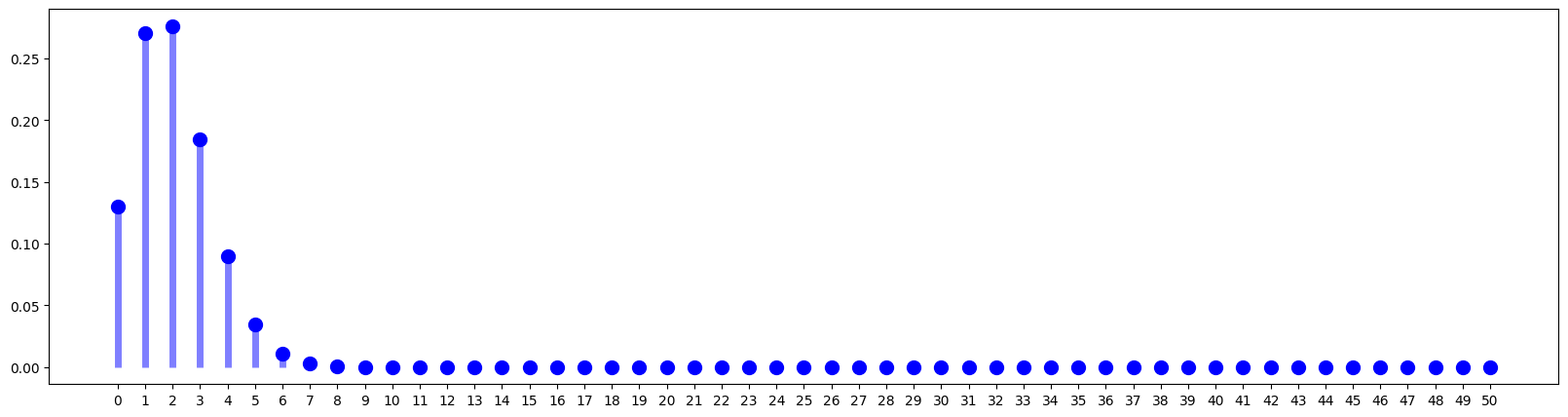

Below is a realization of the PMF of \(Y\):

p = 0.04

n = 50

# our random variable Y

Y = stats.binom(n, p)

y = np.arange(n + 1) # [0, 1, ..., 50]

f = Y.pmf(y) # pmf P(Y=0) P(Y=1)

fig = plt.figure(figsize=(20, 5))

plt.plot(y, f, "bo", ms=10)

plt.vlines(y, 0, f, colors="b", lw=5, alpha=0.5)

plt.xticks(y)

plt.show();

for y_ in range(51):

print(f"PMF for Y={y_} is {Y.pmf(y_)}")

PMF for Y=0 is 0.12988579352203838

PMF for Y=1 is 0.2705954031709139

PMF for Y=2 is 0.27623280740364115

PMF for Y=3 is 0.18415520493576068

PMF for Y=4 is 0.09015931908313288

PMF for Y=5 is 0.03456107231520094

PMF for Y=6 is 0.010800335098500296

PMF for Y=7 is 0.002828659192464365

PMF for Y=8 is 0.0006335017983123325

PMF for Y=9 is 0.00012318090522739773

PMF for Y=10 is 2.1043404643013807e-05

PMF for Y=11 is 3.1883946428808775e-06

PMF for Y=12 is 4.317617745567845e-07

PMF for Y=13 is 5.2586369978069964e-08

PMF for Y=14 is 5.790760979727912e-09

PMF for Y=15 is 5.790760979727948e-10

PMF for Y=16 is 5.278037351314524e-11

PMF for Y=17 is 4.398364459428767e-12

PMF for Y=18 is 3.3598617398414237e-13

PMF for Y=19 is 2.3577977121694196e-14

PMF for Y=20 is 1.5227443557760843e-15

PMF for Y=21 is 9.063954498667164e-17

PMF for Y=22 is 4.978308342070981e-18

PMF for Y=23 is 2.525228869166441e-19

PMF for Y=24 is 1.1837010324217706e-20

PMF for Y=25 is 5.129371140494332e-22

PMF for Y=26 is 2.055036514621123e-23

PMF for Y=27 is 7.611246350448613e-25

PMF for Y=28 is 2.60503967351663e-26

PMF for Y=29 is 8.234320807092859e-28

PMF for Y=30 is 2.4016769020687333e-29

PMF for Y=31 is 6.456120704485886e-31

PMF for Y=32 is 1.5972173617868683e-32

PMF for Y=33 is 3.630039458606517e-34

PMF for Y=34 is 7.562582205430263e-36

PMF for Y=35 is 1.4404918486533809e-37

PMF for Y=36 is 2.500853903912116e-39

PMF for Y=37 is 3.9427876863479427e-41

PMF for Y=38 is 5.620201745890709e-43

PMF for Y=39 is 7.205386853706048e-45

PMF for Y=40 is 8.256172436538177e-47

PMF for Y=41 is 8.390419142823334e-49

PMF for Y=42 is 7.491445663235104e-51

PMF for Y=43 is 5.807322219562096e-53

PMF for Y=44 is 3.8495507137248904e-55

PMF for Y=45 is 2.138639285402722e-57

PMF for Y=46 is 9.685866328816647e-60

PMF for Y=47 is 3.434704371920785e-62

PMF for Y=48 is 8.944542635210379e-65

PMF for Y=49 is 1.5211807202738746e-67

PMF for Y=50 is 1.2676506002282307e-70

mean, var = Y.stats(moments="mv")

print(f"Expected value: {mean}")

print(f"Variance: {var}")

Expected value: 2.0

Variance: 1.92

At this very moment, we can already calculate our the total revenue earned per day and the corresponding profits per day.

This is because we can use the expected value \(\P \lsq Y \rsq\) to get the average number of successful conversion per day.

We see that we are making a loss of \(-2000\) a day.

num_employees = 100

salary_per_employee = 200

revenue_per_successful_call = 90

expected_total_conversions = mean * num_employees

expected_total_revenue = revenue_per_successful_call * expected_total_conversions

expected_total_profits = expected_total_revenue - salary_per_employee * num_employees

print(f"Expected Total Conversions Per Day: {expected_total_conversions}")

print(f"Expected Total Revenue Per Day: {expected_total_revenue}")

print(f"Expected Total Profits Per Day: {expected_total_profits}")

Expected Total Conversions Per Day: 200.0

Expected Total Revenue Per Day: 18000.0

Expected Total Profits Per Day: -2000.0

By theory, we know that increasing either \(n\) or \(p\) will increase the expectation \(\exp \lsq Y \rsq\) since \(n\) and \(p\) are both positive. Consequently, increasing both at the same time will also guarantee an increase in expectation.

So the solutions to increase revenue/profits per day are:

Increase \(n\), the number of calls performed by 1 single employee;

Increase \(p\), the success rate of a call conversion by 1 single employee through techniques like not hard pressing the customers to buy something;

With this realized state of the theoretical (true) PMF, we can employ generative/synthesis method to generate samples from this distribution because we assumed that \(Y\) follows a Binomial distribution prior.

So if we have Y.rvs(size = 10), it simply means generate a sequence 10 random variables \(Y_1, Y_2, \ldots, Y_{10}\) of \(Y\).

We have

In this context, we can be unambiguous and say that each \(Y_i\) should be the number of successful conversion calls made by a single randomly selected employee.

To be more precise, each experiment for \(Y_i\) is like a new randomly drawn 50 calls by a random person, so each time is a realisation of 50 calls from a randomly selected person. So if you have 100 people you can have 100 \(Y_i\). Note the distinction, in \(X_i\), this \(X_i\) is bind to a single person (may be wrong here), here each \(Y_i\) can be any member from the population.

# generate states from binomial distribution

Y.rvs(size = 10)

array([1, 4, 3, 2, 1, 1, 0, 4, 2, 3])

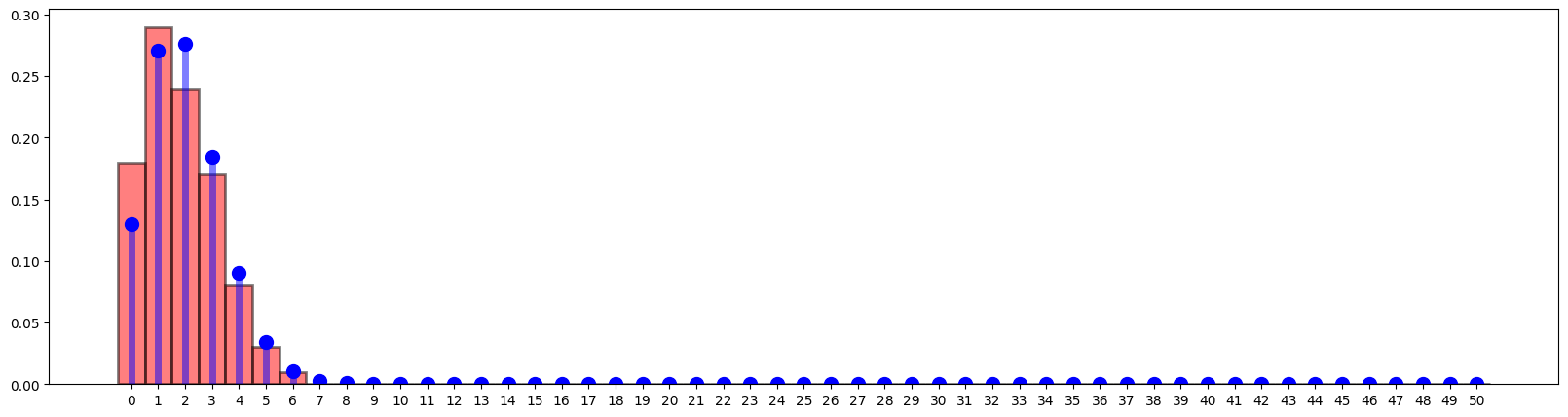

If we plot 100 such \(Y_i\), we form an empirical distribution and compared to the true PMF it has a bit of differences.

bins = np.arange(0, 50 + 1.5) - 0.5

fig = plt.figure(figsize=(20, 5))

plt.hist(

Y.rvs(size=100),

bins,

density=True,

color="red",

alpha=0.5,

edgecolor="black",

linewidth=2,

)

plt.plot(y, f, "bo", ms=10)

plt.vlines(y, 0, f, colors="b", lw=5, alpha=0.5)

plt.xticks(y)

plt.show()

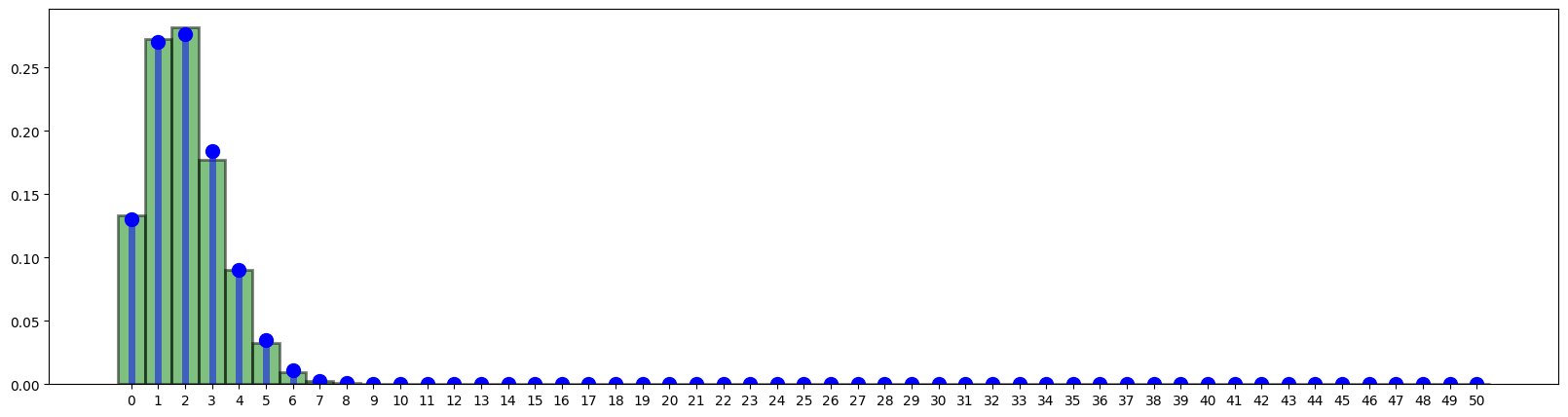

When we increase to 10000, the empirical starts to be closer to the true PMF.

bins = np.arange(0, 50 + 1.5) - 0.5

fig = plt.figure(figsize=(20, 5))

plt.hist(

Y.rvs(size=10000),

bins,

density=True,

color="green",

alpha=0.5,

edgecolor="black",

linewidth=2,

)

plt.plot(y, f, "bo", ms=10)

plt.vlines(y, 0, f, colors="b", lw=5, alpha=0.5)

plt.xticks(y)

plt.show()

Alternative way to Calculate Expected Value of Revenue per Day#

We already know in the long run the company does not earn profits by the law of average (expectation).

We can also calculate it by defining the total revenue as a random variable \(Z = 90Y\) where \(90\) refers to the revenue earned per successful call conversion by an employee.

This means on average, the company earns revenue of 180 per day per employee. Thus if there’s 100 employees, then on average, the total revenue per day is \(180 \times 100 = 18000\), which is the same as we got earlier.

And if we want to further calculate how much the company loses in 1 year, that will be

assuming everything else constant (no employees left etc).

We can also simulate 365 days using code below, we define Z = 90 * Y.rvs(size = 100)

to be the random variable \(Z = 90Y\) (as there is no good way to just use Z=90*Y).

At each loop (day), we get a new draw random variable \(Z\).

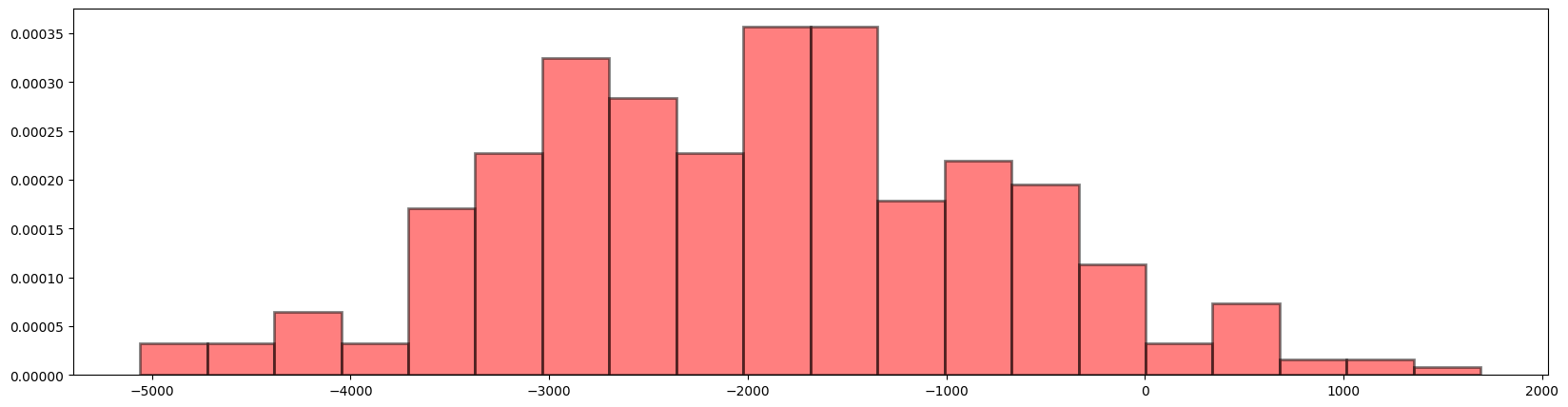

yearly_revenue = np.zeros(shape=365)

yearly_salary_paid = np.ones(shape=365) * 20000

for each_day in range(365):

Z = 90 * Y.rvs(size = 100) # 100 employees' revenue [90, 180, 0, ...]

daily_revenue = np.sum(Z)

yearly_revenue[each_day] = daily_revenue

yearly_profits = yearly_revenue - yearly_salary_paid

#bins = np.arange(0, yearly_revenue.max() + 1.5) - 0.5

fig = plt.figure(figsize=(20, 5))

plt.hist(

yearly_profits,

bins=20,

density=True,

color="red",

alpha=0.5,

edgecolor="black",

linewidth=2,

)

# plt.plot(y, f, "bo", ms=10)

# plt.vlines(y, 0, f, colors="b", lw=5, alpha=0.5)

#plt.xticks(y)

plt.show()

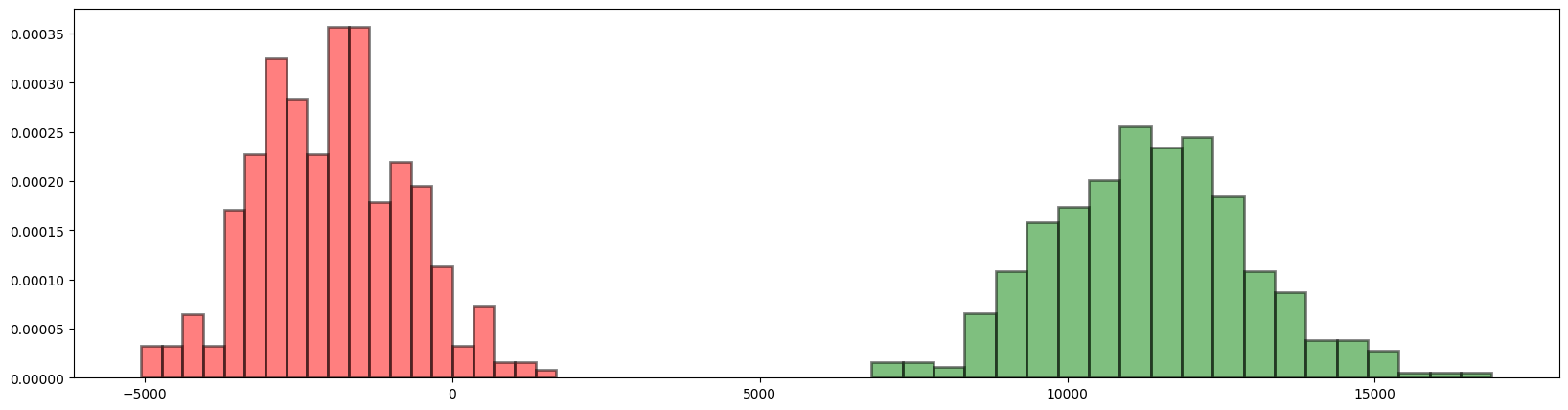

If we increase \(n\) or \(p\), say just bump out both by a bit to \(n=58\) and \(p=0.06\), then we have

p = 0.06

n = 58

# our random variable Y

Y = stats.binom(n, p)

yearly_revenue = np.zeros(shape=365)

yearly_salary_paid = np.ones(shape=365) * 20000

for each_day in range(365):

Z = 90 * Y.rvs(size = 100) # 100 employees' revenue [90, 180, 0, ...]

daily_revenue = np.sum(Z)

yearly_revenue[each_day] = daily_revenue

yearly_profits_improved = yearly_revenue - yearly_salary_paid

#bins = np.arange(0, yearly_revenue.max() + 1.5) - 0.5

fig = plt.figure(figsize=(20, 5))

plt.hist(

yearly_profits,

bins=20,

density=True,

color="red",

alpha=0.5,

edgecolor="black",

linewidth=2,

)

plt.hist(

yearly_profits_improved,

bins=20,

density=True,

color="green",

alpha=0.5,

edgecolor="black",

linewidth=2,

)

# plt.plot(y, f, "bo", ms=10)

# plt.vlines(y, 0, f, colors="b", lw=5, alpha=0.5)

#plt.xticks(y)

plt.show()